VC portfolio companies are often valued through the Recent Transaction Approach.

This method uses the Backsolve Method to estimate value based on the most recent financing round.

But, in a down market where transactions and exits are scarce, relying on past deal valuations can be misleading.

The Discounted Cash Flow Method, may not be reliable as well, given the early-stage nature of these companies. It may be at best a speculative exercise.

A Calibrated Market Approach is another option. It uses the last known transaction price and tweaks it to match the current market. It also considers the company's recent performance and the usual drop in valuation multiples that start-ups face as they grow.

The Calibrated Market Approach considers:

- Compression of Valuation Multiples

- Company Specific Performance and

- Market Conditions

1. Compression of Valuation Multiples

As early-stage companies expand, revenue multiples decrease. This is because future growth expectations lower. The table below shows how valuation multiples have declined, even as revenue and valuations rise and the IPO is done at the market peer multiple.

In the above table, it can also be inferred that the decline in valuation multiple is triggered by declining revenue growth rate.

The subject portfolio company is evaluated considering its revenue stage, number of future fund raise rounds and potential exit valuations.

2. Company-Specific Adjustments

Positive or Negative calibrations may be required in the valuation multiples based on the company’s achievement of closely tracked or agreed upon financial metrics likes ARR, Churn Rates, Net Dollar Retention, Cash Burn and overall financial position relative to the previous transaction.

3. Market Adjustments

Private market valuations do not perfectly track public market movements. A correlation factor adjusts valuations to reflect market trends while accounting for private company dynamics.

Applying the Calibrated Market Approach

Let us understand the application of a Calibrated Market Approach using a practical example:

Company Background:

- Last Funding Round:12 months ago, valued at 40x revenue multiple when revenue was $0.5M, leading to a valuation of $20M.

- Current Revenue: $1.2M (strong revenue growth).

- Revenue Target Missed: 10% miss compared to projections

- Annual Cash Burn: $1.3M, exceeding the initial target of $900K

- Public Market Comparable: Trades at 9x revenue multiple

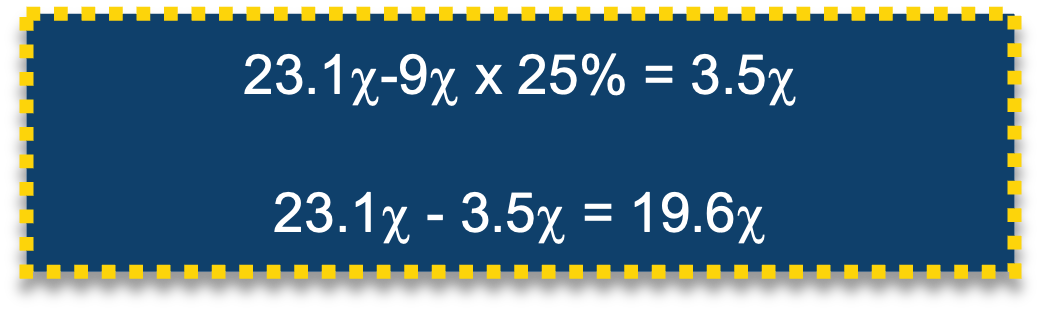

Step 1: Multiple Compression Adjustment

With revenue growing from $0.5M to $1.2M, we compute the multiple compression.

Typically the multiple compression is computed considering a pathway to either a potential M&A exit or IPO and expected rates of returns of various investor classes on such exit event.

For simplicity, we are assuming a 35% compression in multiple.

Applying this:

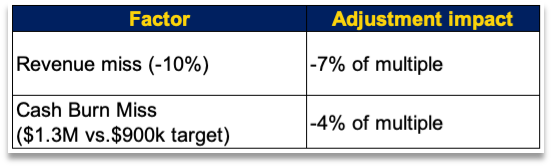

Step 2: Company-Specific Adjustment

The company missed revenue targets by 10% and its cash burn is higher than expected. We apply moderate downward adjustments. This is typically done considering the earlier projections and the expected valuation multiples (post considering multiple compression)

For simplicity, we are assuming the following adjustment impacts

Applying this:

Step 3: Market Adjustment

The public comparable is trading at 9x revenue. However, private companies do not perfectly correlate with public markets, we assume a correlation factor of 75% and hence non-convergence by 25%. Practically, this factor is assessed using data from pre-listing valuation multiples with listed valuation multiples.

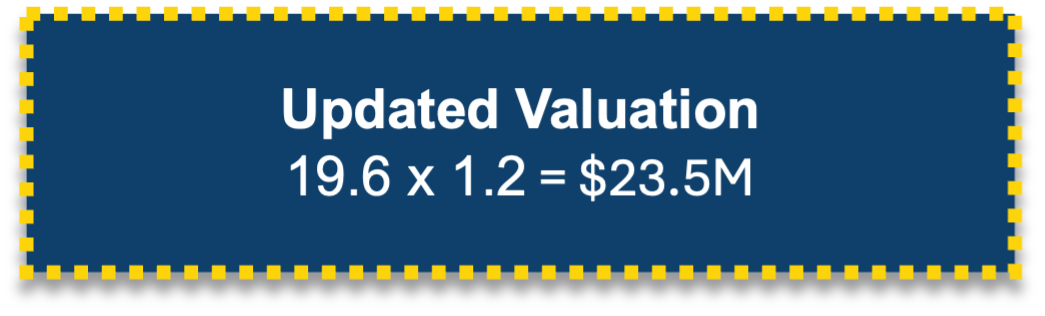

Final Valuation Calculation

- Final Adjusted Multiple = 19.6x

- Current Revenue = $1.2M

Why VCs Should Consider Calibration?

This approach bridges the gap between past valuations and evolving market realities. The AICPA’s valuation guidelines to value of portfolio companies also suggest adoption of Calibration as it aligns valuation models with initial transaction assumptions and updated inputs over time based on company performance and market conditions.